The most influential economist of the late 20th century, Milton Friedman, had a revolutionary effect on today’s world. The turn of 1980 marked a rebirth of economic liberalism and monetarism, a departure from the misguided stop-go monetary and Keynesian fiscal policies. The work of Friedman gave free market leaders in Reagan and Thatcher the framework to espouse their ideals, with the former particularly turning to Friedman for policy advice. The breakdown of monetarism’s credibility in recent decades culminated in the aftermath of the Financial Crisis. Friedman’s famous quote, “Inflation is always and everywhere a monetary phenomenon,” appeared to no longer hold as excessive quantitative easing failed to produce subsequent increases in the price level or GDP following the Great Recession. Though Friedman’s espoused fiscal policies have had long lasted success with the triumph of free-market capitalism over the Soviet Union, producing a further turn towards the neoliberal ideals of Friedman, emerging fallacies in his monetary views have promoted the rise of market monetarism as a successor to monetarism.

Quantity Theory of Money

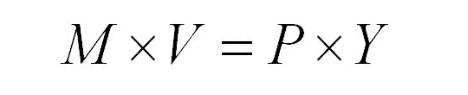

Developing on the ideas first espoused by Irving Fisher, Friedman produced the Quantity Theory of Money law. In all instances, nominal GDP (right-hand side) is equivalent to the money supply (M2) multiplied by the velocity of money. Friedman further built on these ideals by researching money’s velocity, concluding that it is constant in the long run.

As a result, Friedman’s Quantity Theory of Money stated that increases in the money supply result in nominal GDP growth. By extension, inflation was always a monetary phenomenon!

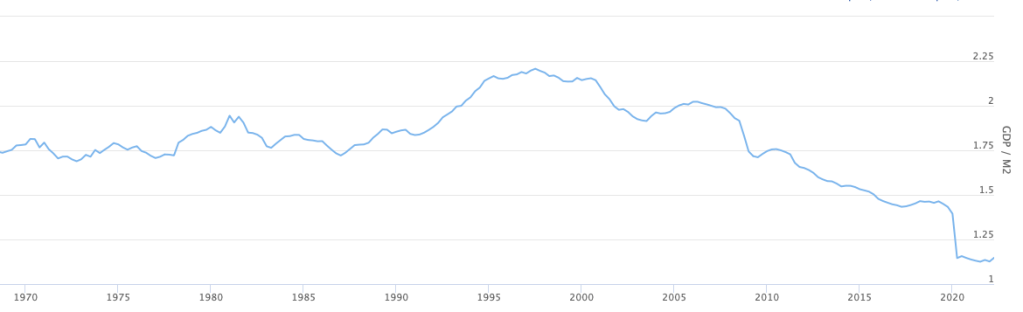

However, this relationship began to break down following the Financial Crisis of 2008. Considerable increases in quantitative easing were followed by both the Federal Reserve and Bank of England, ushering in a wave of stimulus and increasing the narrow money supply. Despite this, inflation remained stagnant, falling to 0% by 2015.

This fall is because of the sharp decline in the velocity of money. As institutional investors and consumer pessimism rose following the Financial Crisis, the unwillingness to move capital and the tendency to save decreased the money velocity. By 2017, money velocity reached record lows not witnessed since the late 1940s – the end of WW2.

Subsequently, money supply growth wouldn’t produce a proportionate increase in nominal GDP. However, both Central Banks rapidly accelerated expansionary open market operations (notably Quantitative Easing) to more than compensate for the sharp slowdown in velocity; yet, these adjustments still failed to stimulate substantial increases in inflation. The increased regulatory burden played a part in this.

Regulatory Burdens

The financial crisis undermined Friedman’s Quantity Theory of Money through greater regulatory oversight. New rules, introduced to curb speculation, drove the demand for government bonds. Gone were the days of derivatives; under the guise of government intervention, pension funds and institutional funds globally were now forced to hold large quantities of bonds. Higher demand for bonds caused the interest rate to fall (and subsequently the price level to fall for money market equilibrium).

As financial institutions were required to purchase increasing bonds, the money demand for bonds rose, resulting in falling yields. Through this portfolio rebalancing effect, the increase in demand for bonds would provoke a subsequent fall in bond yields and interest rates throughout the economy.

The fall in interest rates leads to excess demand for money. Given that the Central Bank wants to offset deflationary effects on the economy from higher bond and money demand, money supply growth increases.

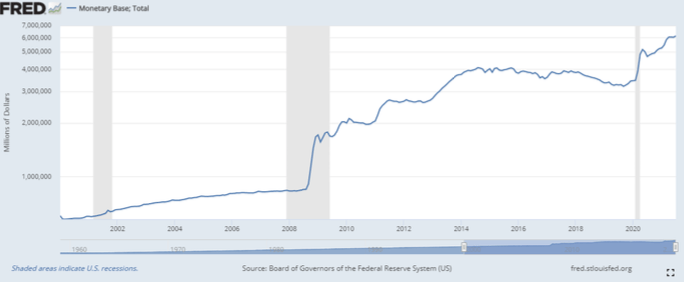

The Central Bank must therefore increase the money supply accordingly to supplement the increased demand for base money (M0) as a result of higher bond demand from higher risk aversion and regulatory burdens. Hence, the surge in the monetary base was necessary to complement the excess demand for money. Had neither Central Banks taken to quantitative easing, the increased regulations and uncertainty would’ve had a deflationary effect on the economy, as financial institutions poured money into bonds, provoking a sharp fall in the velocity of money.

Fixed Monetary Rule

In many ways, Friedman’s fixed monetary rule was an extension of his Quantity Theory of Money conclusions. He argued that Central Banks should increase the money supply according to the level of GDP. For example, if an economy grows 2% in a given year, the Central Bank should increase the money supply by an equivalent amount to avoid the inflationary effects of excessive money supply growth. There are several issues with Friedman’s hypothesis.

- Velocity cannot be assumed constant in the long run. An increase in the money supply won’t necessarily produce a proportionate increase in GDP.

- Monetary policy has a significant time lag. The market conditions of one year may differ from the next (due to a sudden shock), which would require a sharp increase in the money supply to counteract rising/falling inflation expectations. This was seen in the lead-up to the financial crisis as the Federal Reserve enacted contractionary measures by slowing the rate of M2 growth and raising the federal funds rate to counteract rising inflation from oil prices (appreciating the currency to make oil imports cheaper), provoking a decline in aggregate demand. This was despite core inflation largely unaffected, leading to rising inventory:sales ratio, prompting a sharp fall in output and a recession.

- Debt increases exponentially with interest. Friedman’s rule suggests a 0% inflation target is optimal. However, as banks don’t reinvest all interest income into the economy, this creates a shortage of money available for debt repayment (debtors have to repay the loan amount + interest). Inflation through money supply growth is therefore required to inflate away this debt, to prevent excessive defaults and bankruptcies.

- Zero inflation promotes economic rent. Money should be used as a financial tool for transactions, or to finance entrepreneurs (risk taking on capital). A lack of inflation incentivises large saving, weakening the economy through a slump in velocity.

Ultimately, Friedman’s primary monetary assumptions failed to hold true in the 21st century. His assumption that velocity was constant in the long run unravelled amidst the Financial Crisis with increasing regulations and risk aversion forcing financial institutions into the bond market. Forcing Central Banks to increase the money supply to complement the excess money demand caused by lower bond yields and interest rates, money velocity continued to fall. With this said, Friedman’s contribution to economics cannot be understated. The importance of the establishment of a clear link between inflation and the demand-side of the Central Bank’s monetary policy cannot be understated, breaking from the Keynesian, stop-go statusquo that plagued the late-1960s and 1970s.