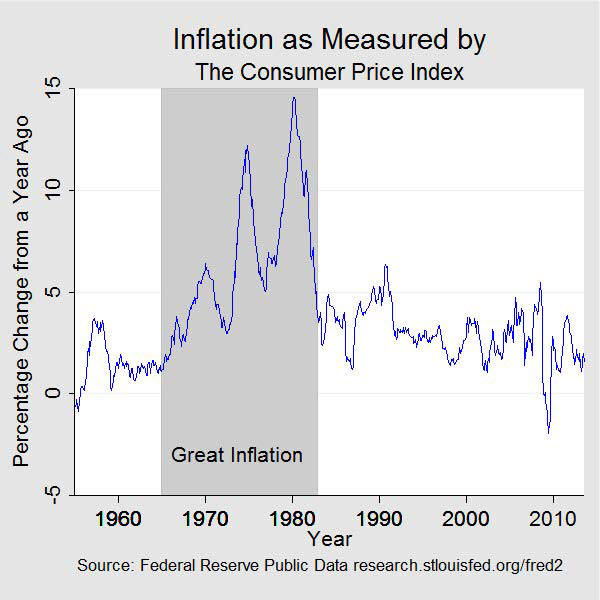

Inflation. Squeezing millions of households across the UK to the brink. Excessive stimulus by Central Banks globally, particularly the Federal Reserve and the Bank of England, have exacerbated supply side shocks. Economists likening the inflationary shocks of the 1970s are misguided. The Great Moderation, the three decades of economic stability and growth that succeeded the years of stagnation, marked a departure from failed Keynesian policies. Central Banks look poised to reduce inflationary pressures – at least on the demand side of the equation.

Supply & Demand shocks

Inflationary pressures can arise from either supply or demand shocks within an economy. External supply shocks through rising commodity prices result in cost-push inflation – reducing short-run aggregate supply. Expansionary monetary stimulus, holding real interest rates below market interest rates, can produce demand-pull inflation – aggregate demand rising above the productive potential of an economy.

Unfortunately, most Western economies are experiencing both supply and demand-side inflation. Although monetary policy has limited effect on the supply-side of an economy, Central Banks have complete control over the demand-side and can introduce contractionary measures to stem demand-side inflation and raise interest rates above the market rate, taming inflation expectations in the process. However, these measures shouldn’t be overly excessive – a mistake Central Bankers in the 1970s repeatedly made.

Manipulating the Output gap

The stagflation crisis was primarily a result of Central Bank output gap manipulation; a policy since termed ‘stop-go.’ By drastically contracting nominal output through sharply reducing money supply growth, Central Banks in the US and UK made the same mistake of causing mass unemployment. The introduction of contractionary measures in the first place was a mistake. Initially, inflationary pressures arose due to a sharp rise in oil prices during 1971. As Central Banks have little influence over temporary, external supply-side shocks, policymakers shouldn’t manipulate aggregate demand to lower these pressures. Nevertheless, both the Bank of England and the Federal Reserve sharply reduced money supply growth, inducing unemployment.

As unemployment rose, inflation fell. However, as officials oversaw rising unemployment, heavy political pressures quickly induced Central Banks to reverse their contractionary measures. The Federal Reserve promptly changed course following the unemployment spike of 1975, increasing money supply growth to 14% in 1976-78. A sharp reversal from the 5% money supply growth of 5% during the previous two years provoked a sharp rise in inflation. The same phenomenon was too witnessed in the UK. Both Central Banks continually repeated their mistakes. A sharp increase in the money supply led to a positive output gap (aggregate demand exceeding the long-run aggregate supply of the American economy – full employment), resulting in inflationary pressures. A sharp contraction in the growth rate of money followed, leading to a negative output gap (aggregate demand falling behind aggregate supply), producing high unemployment.

This stop-go monetary policy cycle lasted until 1980. Paul Volcker became the chairman of the Federal Reserve in 1979 and set out a clear agenda to gradually reduce the rate of money supply growth. It is essential to recognise that money velocity was relatively constant during this period – allowing us to attribute the inflationary pressure solely due to the money supply. This is unlike following the Great Recession, as money supply growth didn’t produce inflationary pressures due to a sharp rise in money demand.

Ultimately, the era of stop-go monetary policies led to a decade of stagnation. Price volatility prevented the price mechanism from allocating resources efficiently, raising uncertainty in inflation expectations and producing an unstable investment environment – limiting long-run economic growth. Through extreme fluctations in money supply growth, both the UK and the US experienced high levels of unemployment and inflation across the decade. Only once both nations established inflation targeting did unemployment and inflation stabilise – although this policy brought about many other issues.