‘Tax cuts for the rich!’ A cry consistently echoed by those against reducing top tax rates. ‘Trickle-down economics,’ a phrase first uttered by President Franklin Roosevelt in the depths of the Great Recession, despite no economist in history supporting this line of reasoning. Unfortunately, the facts suggest otherwise. Reducing top tax rates from punitive levels, has in almost all cases, boosted tax revenue and produced higher employment levels, producing economic growth and prosperity.

1920s: Tax Cuts & Growth

The top tax rate stood at 73% in 1924; by 1929, this had fallen to 24%, between unbridled economic growth and prosperity.

From 1916 to 1918, the number of higher-rate taxpayers (those on the aforementioned 73% rate) fell by half. Hardly the coincidence of a disappearance of wealth, the emergence of tax-exempt securities – municipal bonds, provided a haven for wealthy individuals. While middle-income earners lack access to accountants and consultants that can appropriately use and manipulate the tax code in their favour, high-income earners avoid paying higher taxes. Private activity bonds, another security exempted from income taxes (even in 2022), are issued to raise capital for a ‘private project’ – in most cases, a project established by said individuals.

Secretary of the Treasury, Republican Andrew Mellon, attempted to end this unfair treatment in the early 1920s following the Republican accession to power. Met with fierce resistance from congress, following President Coolidge’s election, Mellon took to tax reductions. Crucially, cutting taxes shifted capital from the government to the private sector. As a pose to the wasteful spending by bureaucrats, the private sector efficiently allocated resources according to consumers’ preferences, spurring long-run economic growth.

A common misconception was addressed during this period. Tax revenues ROSE in the years following the sharp income tax cuts. As an increasing number of wealthy individuals found it cheaper to pay taxes instead of paying for accountants to cut the tax burden, the incentive structure to package earnings via tax-exempt securities (nowadays in the form of tax havens) broke down. Coupled with the economic growth from greater allocative efficiency from tax cuts, unleashing enterprise and productivity through investment, the counter-intuitive of higher tax revenues should not be a surprise.

Post-WW2 era

Faced with large government debts after WW2, the US raised the top tax rate to levels above 80% for the better part of three decades. However, the effective tax rate was far lower, estimated at around 40-50%. Extensive tax deductions and relief made it easy for high-income individuals to avoid the headline top rate – a common theme in 21st-century Western nations. Instead of drastically simplifying the tax code to prevent tax avoidance, successive governments continued adding loopholes and deductions.

The election of Kennedy in 1960 was a tightly fought battle. Looking to boost economic growth, JFK proposed a tax reduction plan that eventually passed following his assassination. The headline top rate fell from 91% to 65%, with corporation tax falling from 52% to 48%. Income tax reductions were introduced for all income groups, and many tax deductions and loopholes were eliminated. While projections predicted income tax revenues would fall by $10 billion, revenues increased each year after its passage in 1963.

Similar to the 1920s, the Kennedy tax reductions saw increases in economic growth through a more efficient market allocation of resources. Unemployment fell from 5.2% in 1964 to 3.8% by 1966. Unfortunately, President Johnson later raised taxes in 1968 to close the budget deficit from his newly introduced welfare promises, coinciding with a colossal surge in monetary stimulus, giving birth to the stagflation of the 1970s.

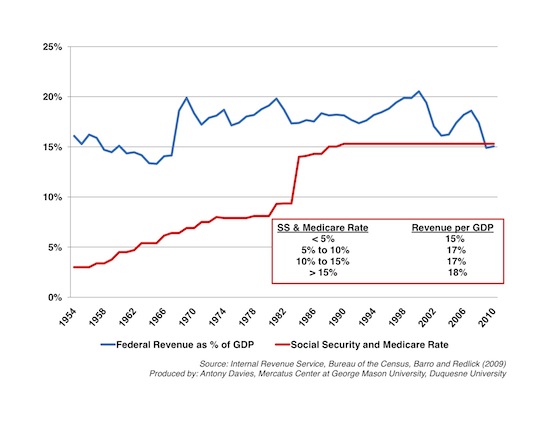

Tax & Revenue

The increase in tax revenues between 1962 and 1968 coincided with a sharp fall in tax revenue per GDP due to the sharp rise in economic activity, promoting prosperity. Lyndon Johnson’s tax rises in late 1968 marked an end to this.

Neoliberal era

The Neoliberal revolution of the 1980s saw top tax rates fall in both the UK and the US; tax revenues in both nations increased. The basic income tax rate fell from 33% to 23% under Conservative rule in the UK. A common misconception of the growing budget deficit under Reagan was from a shortfall of tax revenues; the reality was that a surge in military spending ballooned the deficit while revenues increased.

The Socialist government of the 1990s in France instituted a wealth tax – increasing progressively on assets worth above €1.3m from 0.5% to 1.5% on assets above €10m. Unsurprisingly, the result was contrary to expectations. French economists have concluded that the tax cost France twice the revenue it raised. Ten thousands households with approximately €35 billion worth of assets left France between 2000 and 2015 due to such a tax. This deprived France of the necessary capital required to promote economic strength. Thankfully, President Macron learned from these past mistakes, abolishing the wealth tax shortly after his election in 2017. Coupled with labour reforms, Macron lowered the youth unemployment rate from 25% to 15% and produced the lowest unemployment rate since the 1970s – thanks to neoliberal reforms.

Ultimately, supposed ‘tax giveaways’ for the wealthy and corporations have produced rising living standards and prosperity. The Coolidge, Kennedy and Reagan tax cuts produced rising tax revenues – contrary to expectations. A more efficient market allocation of resources, limiting tax avoidance by making it more profitable to invest, and rising productivity produce economic growth that boosts tax revenues in the long run.