What promised a refreshing start for Britain has since ended in disaster. Truss campaigned to revitalise our stagnant economy, ripping back regulations, and transform Britain from a high-tax, low-wage economy to one of low taxes and prosperity. The markets rejected a wholly un-conservative budget from Kwasi Kwarteng, leaving a collapsing pound and forcing the Bank of England to intervene temporarily. A desperate Truss sacked her chancellor before being forced to resign only a week later. As the Conservative Party inevitably faces a decade of political wilderness, learning the lessons from her distraught premiership is vital to restore the stagnant British economy to Kwasi’s vision of Thatcher’s lasting legacy.

Kami-Kwasi Budget

Kwarteng promised a market economy only to have his ‘mini’ budget rejected by the market.

Cameron’s austerity program was enacted in the name of fiscal rectitude. Ascending the premiership with a £140 billion deficit, a higher proportion of the economy than Greece at the time, the coalition sought fiscal restraint to reassure the markets that the UK’s debt was sound. This involved difficult decisions that proved politically unpopular. However, by 2019, the government had balanced the books and kept interest rates low, leading to the second fastest-growing economy in the G7 across the decade. Kwarteng’s budget shattered a decade of fiscal prudence.

Despite the record of solid growth, the Conservatives saw a raft of profound structural issues within Britain, such as stagnant productivity and incomes. Kwarteng’s supply-side reforms attempted to address these directly, slashing the top income tax to a competitive rate of 40%, cancelling the National Insurance tax rise, and loosening housing regulations. In rather unconservative fashion, Kwarteng’s budget unleashed a deficit of $65 billion annually. Under Sunak’s previous plans, the deficit was set to fall as a proportion of GDP by 2024; had Kwasi’s budget been implemented, projections forecasted Britain’s debt to GDP to rise indefinitely.

Without the world’s sovereign currency, a growing deficit wasn’t economically palatable, leading to the markets reacting violently against the pound and gilts. A failure to establish a balanced plan to couple the tax cuts and supply-side reforms with spending reductions and efficiencies led to calamity and his inevitable downfall. Destroying the Conservatives’ reputation of fiscal responsibility will take decades to recover.

Structural Shortfalls

Whether Sunak or Johnson takes to the helm of the Conservative Party, it is unlikely that Britain’s deep-seated structural problems will see resolution. Growing dependency culture, low productivity growth and limited investment are severe strangleholds that limit Britain’s productive potential. In 2021, 5.7 million individuals claimed universal credit – the highest proportion of the adult population in Europe.

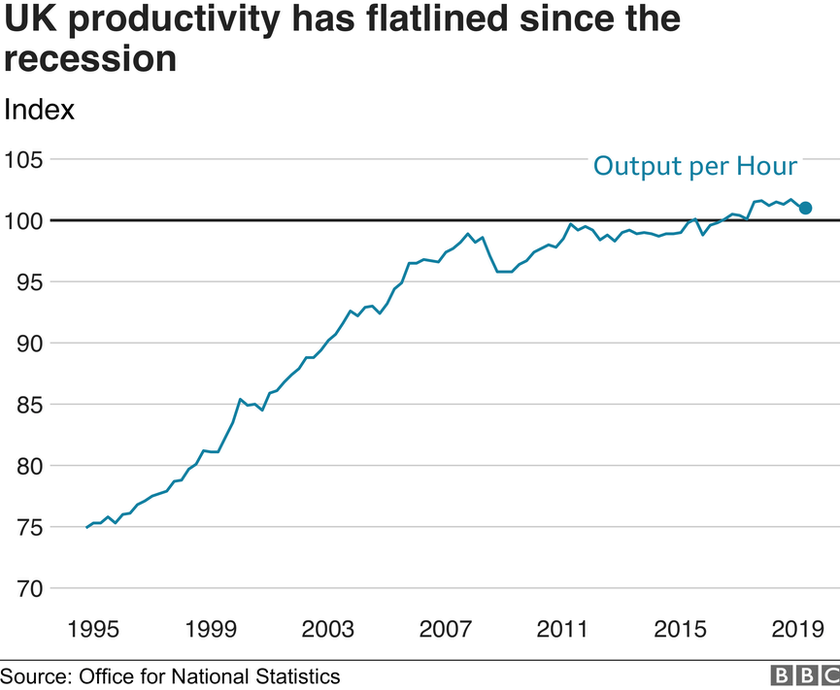

The productivity gains of the 1980s, 1990s and 2000s that brought us closer to France and Germany haven’t continued in the 2010s. Productivity has essentially flatlined since the financial crisis. Starting with Labour’s Alistair Darling, successive governments have slashed capital investment.

Structural failures of the British economy are primarily to blame. In 2016, the UK ranked 35th out of 36th for how heavily capital investments are taxed. Under the coalition, Osborne eliminated significant deductions for investments; Cameron eliminated deductions for industrial building development from 58%. As such, while the headline corporation tax rate in the UK fell from 28% to 19%, the effective corporate tax rate rose. Heavily taxing businesses limits investment. Unsurprisingly, the UK in 2019 had the lowest share of investment in the G7 at 10% of GNP. As the corporate tax rate looks set to rise to 25%, the severe lack of business confidence in the UK is surprising to few as Britain looks to tax its way to growth.

Kwarteng proposal of reversing the corporate tax rise would merely be a continuation of the status quo. The proposal to cut the basic income tax rate from 20% to 19% blew up the budget deficit – yet, it would’ve done nothing to improve the supply side of the economy. A rising budget deficit results in higher interest rates, choking off the private sector through higher borrowing costs. Any attempt to shrink the state through tax cuts must be accompanied by spending reductions, as rising deficits and subsequent interest rate hikes undermine any attempts to promote private sector growth.

Drastic action is required to solve the ongoing productivity crisis. The ascension of Hunt to the chancellorship will do little to promote productivity growth. Continuing with the corporate tax hike won’t encourage businesses to invest in the British economy. Without significant tax reform, global Britain will continue to sink into the abyss.

Ultimately, the failure of Trussonomics coincided with a failure to grapple with the structural issues facing the British economy. A growing budget deficit startled the market, resulting in the pound’s collapse. The most notable shortfall – a lack of productivity growth was hardly addressed by Kwarteng. A reversal of the corporation tax increase is a continuation of the status quo – far from a radical proposal to shrink the state. As deficits are funded by the private sector, slashing taxes without proportional spending cuts wouldn’t promote the boom in private sector activity that Kwasi hoped. An inevitable return to status-quo economics with Jeremy Hunt will seal Britain’s fate as the next Italy of Europe.