The Global Financial Crisis of 2008 birthed a wave of unorthodox expansionary monetary policy measures. Quantitative easing sought to lower bond yields, pushing financial institutions into riskier assets and thereby increasing aggregate demand; similarly incentivising banks to resume lending, shoring up their balance sheets as bond prices soared. The reality was more complex. Highly levered financial balances severely restricted the capabilities of banks to resume credit flows – the levels of Quantitative Easing weren’t sufficient to match the levels of money destruction and loss of confidence in Western economies.

Post 2008

Quantitative easing ushered in open market operations on an unprecedented scale without its intended consequences.

Amidst a sharp liquidity crunch following the collapse of the sub-prime mortgage crisis, interest rates quickly hit the zero lower bound; despite this, lending failed to return to pre-crisis trend with Central Banks turning to quantitative easing – the purchase of long-term, government debt in an attempt to stimulate aggregate demand through increasing the money supply. However, this failed to come to fruition as money velocity sharply fell. Financial institutions were deleveraging and thus didn’t have the financial capacity to increase lending.

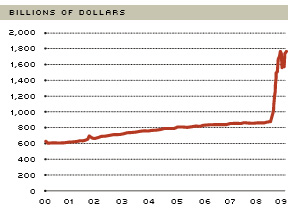

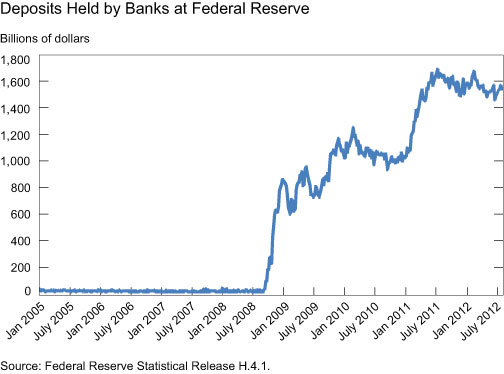

Paying interest rates on excess reserves exacerbated the issue. In 2008, the Federal Reserve announced it would pay 1.4% on required reserves and 0.7% on excess reserves. This has a hugely contractionary effect on the US economy – rendering it more profitable for banks to deposit reserves at the Federal Reserve as a pose to increasing lending.

As loans’ profitability constrains banks, quantitative easing increases won’t spur lending unless it is more profitable to loan instead of alternative investments: purchasing bonds or parking deposits at the Federal Reserve.

Additionally, the collapse of mortgage-backed securities restricted lending by reducing banks’ assets’ value. Loans need to be backed with assets due to capital requirements. If the value of a bank’s assets falls – as occurred with the destruction in the value of MBSs, this severely restricts the capability of banks to loan money. Weakened consumer confidence further reduced the demand for loans, contributing to the fall in aggregate demand that followed 2008 in most Western economies.

Ultimately, quantitative easing couldn’t effectively spur economic growth following the Great Recession due to the severely leveraged framework. The collapse of mortgage-backed securities destroyed the asset sheets of previously profitable retail and commercial banks, restricting their ability to create credit. Coupled with the introduction of interest on excess bank reserves, banks were further disincentivised to loan money. The nominal income recovery finally came in 2013 following an additional $1 trillion in stimulus by the Federal Reserve, increasing consumer confidence and putting financial institutions in the position to continue credit creation following its five-year hiatus.