John Maynard Keynes revolutionised the Economics profession. Through developing the foundations for the New Keynesian consensus that occupies policymakers today. However, successive Labour and Conservative governments stuck religiously to the Keynesian demand-management model, neglecting the supply-side performance of the economy that continuously lagged behind its peers. Heavy government intervention, a key tenant of the original Keynesian framework, led to severe misallocation of resources, leading to relative decline. Only in 1979, Thatcher’s election marked an end to the managed decline as her economic reforms revitalised the stagnant British economy.

Demand-Management Economics

Clement Attlee’s tenure starting in 1945 marked the start of the managed decline. The UK had severe structural problems following WW2; a chronically under-skilled workforce coupled with areas of extreme poverty required investment in long-term skills training to boost the economy’s productive potential. Instead, successive governments devoted resources to establishing a comprehensive welfare state. While well-intentioned, Britain’s severe structural shortfalls required extensive, long-term investment to maintain its competitiveness globally. The welfare state crowded out resources that should’ve gone into education and industrial development. The UK’s primary pre-WW2 competitors in Japan and Germany were left decimated, leaving both the UK and the US as the primary sources of industrial output for the West. As both Labour and Conservative governments became complacent, these economies recovered and eventually became far more competitive and wealthier than the UK.

Throughout the 1950s and 60s, successive governments worked closely with trade unions and industrial sectors to maintain full employment at all costs. Among many with heavy-state involvement, management of iron, steel and shipbuilding industries was left powerless as the workers resisted changes to working practices that would’ve boosted productivity and efficiency. Britain became a laggard in the global economy. Government contracts were guaranteed regardless of output and efficiency; legislation favourable to unions restricted innovative working practices and guaranteed jobs irrespective of production quality. Britain’s economic performance unsurprisingly declined. Politicians focused on employment, neglecting the economy’s supply side that suffered under these restrictive conditions.

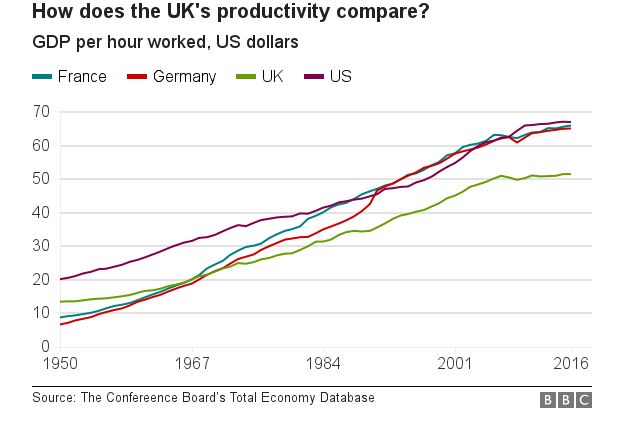

Real GDP growth in the UK lagged behind its peers. Between 1950 and 1979, the UK economy grew at an average of 2.3%; by comparison, this figure was 4% in France, and 5% in Japan and Germany. Similarly, productivity and GDP per capita quickly fell behind.

The 1970s marked a turning point for the British economy. The power of unions led to real wages far exceeding the marginal revenue product of labour, creating an inflationary cycle as the economy operated beyond its productive potential – backed by both Heath and Callaghan governments. Industries such as manufacturing were overstaffed due to the limited power of management and unions guaranteeing jobs for workers regardless of output, creating huge losses as both steel and shipbuilding industries represented sharp losses for taxpayers. In 1974, British steel was 40% less productive than its German counterparts. Struggling with a combination of a lack of competitiveness and inevitably growing losses, this became unsustainable for British governments. Governments inevitably introduced pay freezes to stem the spiralling inflation that resulted from workers paid beyond their productive capacity, producing strikes and industrial action that grinder the economy to a halt – further worsening the inflationary crisis. Firefighters in 1978 held the public hostage by demanding a 30% annual pay rise, far exceeding the inflation rate. Britain became the sick man of Europe.

Thatcher

The Conservatives won in 1979 with a promise to end the terminal decline that started in the 1950s and was crippling the economy by the 1970s. Union legislation passed in the 1980s curbed their power, allowing management to make the necessary changes to boost output and working standards. Loss-making industries were no longer subsidised by taxpayers, privatised and left to the free market to end the misallocation of resources that many industrial sectors represented. Corporate taxes were lowered from 52% to 35%, eliminating deductions that led to less productive economic investments. Income tax cuts similarly redistribute more resources to the private sector, leading to further productive potential growth and allocative efficiency. Surplus labour in many of these industries was fired, leading to a boom in the British economy as resource allocation improved.

Manufacturing productivity rose 40% between 1981 and 1986 – a sharp contrast from the 0.2% gain during the 1970s. The UK boasted the fastest growing economy out of Japan, Germany, the US and France during these years. Real median income growth and productivity growth similarly exceeded these Western nations during this period. The productivity gap between the UK and its Western counterparts began to narrow, as Germany fell from 2.5x to 1.8x as productive as the British economy.

Ultimately, the sluggish economic growth and declining competitiveness from the 1950s to 1979 are attributable to the severe misallocation of resources imposed by excessive government intervention. Heavy union control, particularly over manufacturing industries, led to a sharp fall in global competitiveness, preventing better working practices from being introduced by management and leading to a less dynamic economy. Thatcher turned the British economy around – from the sick man of Europe to an economic power once again revered globally.