Following the Financial Crisis of 2008, Western financial systems have been subject to much political debate. Severe misallocations of credit in the years leading up to the subprime mortgage led to excessive housing construction and speculation, culminating in a financial catastrophe. With this said, the role of large commercial and retail banks particularly hasn’t been called into question, with investment banks taking the brunt of the blame. This view is misguided as the former played a significant role in the inefficient, allocative excess and, similarly, the sharp rise in asset-price inflation in the years since. The five largest retail and commercial banks in the UK hold over 90% of deposits; is this an economic system that could do with substantial restructuring?

Credit Creation

Types of bank credit: Consumption, Financial & Investment

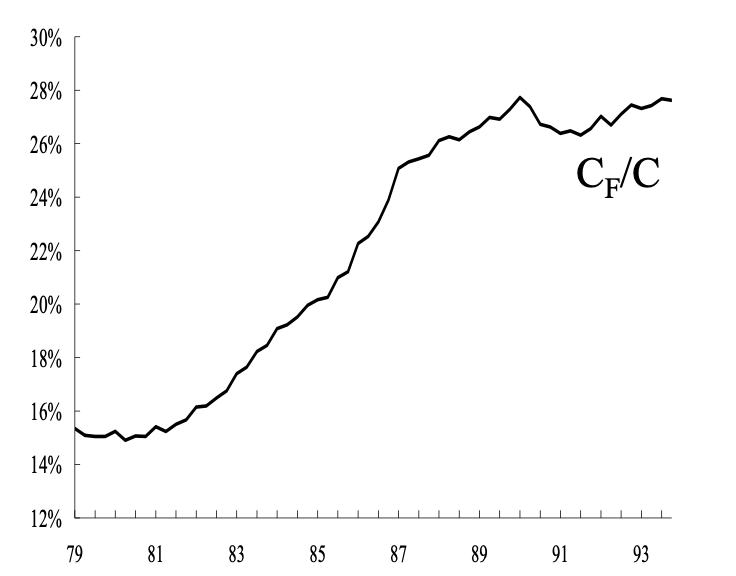

Commercial and retail banks are responsible for increasing the money supply by issuing and allocating credit. Distinguishing between the types of credit allocation is crucial to understand the efficiency of an economy. Financial credit neither constitutes nor increases real GDP; this type of credit allocation is highly unproductive and leads to asset bubbles. There is an opportunity cost to allocating credit to unproductive financial assets; productive industries receive less support. The Japanese economy is a prime example of this phenomenon.

The number of loans to real estate, construction and non-bank financial institutions rose sharply during the 1980s. This led to a huge surge in asset prices, despite little changes in their quality – an asset bubble. When speculative credit creation started falling, Japan quickly went into recession.

Broad credit growth produces asset and financial bubbles that culminate in financial crises. This occurs when bank credit creation exceeds nominal income growth, producing asset-price inflation. As banks exist for profit purposes, efficient allocations of credit aren’t prioritised; fuelling productive investments may not be as profitable as fuelling speculative excess in the short term. Credit controls are the most effective way to ensure banks don’t fund speculative activities through issuing financial credit.

Quantitative Credit Guidance

A common policy in Asian economies during their rapid economic growth, credit controls ensure an efficient allocation of credit by preventing banks from fuelling speculative excess. Previously rejected in Western economies as ‘distorting the free market,’ these act as a crucial tool to ensure credit is efficiently allocated for productive, long-term means. While theoretically , these neo-classical assumptions hardly apply in reality as incentive structures lead banks to prioritise short-term profits that may otherwise be harmful for the economy in the long term.

Similarly, reshaping the structure of the financial sector with smaller banks will achieve the same purpose. In Germany, 70% of deposits are with non-profit/locally small banks. Empirical research supports the notion that large banks tend to lend to large firms, whereas small banks lend to small firms. Establishing a more competitive banking sector with numerous smaller banks will ensure SMEs receive productive allocations of credit. As smaller banks lack the incentive to fund speculative credit allocation, credit is more efficiently allocated under decentralised banking regimes.

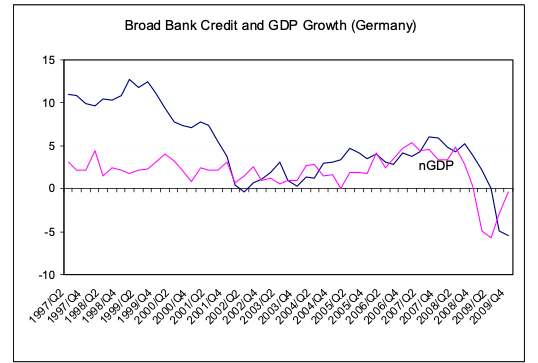

Through efficient credit allocation, Germany avoided the sharp economic downturn that most Western economies faced in 2008; the absence of a housing bubble coupled with smaller banks willing to lend to SMEs prevented the boom-bust cycle from occurring in Germany. In the UK and US where small firms were credit-restrained in the years during and after the credit-crunch of 2008; this wasn’t the case in Germany due to its competitive, small banking sector. German exports from SMEs are similar to that of China, despite having less than 7% of the its population – an indication of successful credit allocation as Small and Medium-Sized enterprises aren’t starved of credit.

Ultimately, efficient allocations of credit are integral to a successful economy. As private banks have failed in this regard, producing spectacular asset bubbles through short term, profitable financial credit allocation, the need for financial sector reform across much of the West is evident. A more competitive banking industry with smaller banks responsible for credit allocation is one way of achieving this – with its success in Germany in restricting broad credit growth to nominal income growth, crucial in preventing a deep recession during the Global Financial Crisis of 2008.